IGas site at Misson Springs, 28 January 2019. Photo: Eric Walton

IGas has confirmed its first shale gas well at Springs Road in north Nottinghamshire has reached its total depth of 3,500 metres and encountered all three targets.

Company accounts for 2018 published today also revealed:

- Loss after tax of £21.4 million

- Doe Green in Warrington exploration written off as not commercial

- Sale of licences in East Midlands and Weald looks unlikely

- Increased revenues mainly because of higher oil prices

- Increased cost of sales because of higher production and transport costs

- Constraints on production from water disposal in the east midlands and the weald.

- £8.1m investment in gas-to-grid project, water injection and site upgrades

- £2.5m investment in shale development programme, including Ellesmere Port appeal

IGas chief executive, Stephen Bowler, said:

“there is still significant upside in our conventional portfolio and we look forward to bringing projects to final investment decision over the coming months.

“We are delighted with the initial results of our appraisal campaign in the Gainsborough Trough having recovered high quality hydrocarbon bearing cores at our Springs Road site.”

Key updates

Springs Road, Misson, Nottinghamshire

IGas said the well, spudded on 22 January 2019, encountered its three target formations of the Bowland Shale, Millstone Grit and Arundian Shales.

The well also recorded a sequence of hydrocarbon-bearing shales measuring more than 250m in the upper and lower Bowland shales. Gas indications were also observed in the Millstone Grit sequence, deeper in the lower Bowland shale and in the Arundian shales, the accounts added.

The company said:

“The cores and wireline logs will now undergo a suite of analysis, the first results of which should be available in the second quarter of 2019.”

Drilling performance was better than expected and costs were lower, the accounts added.

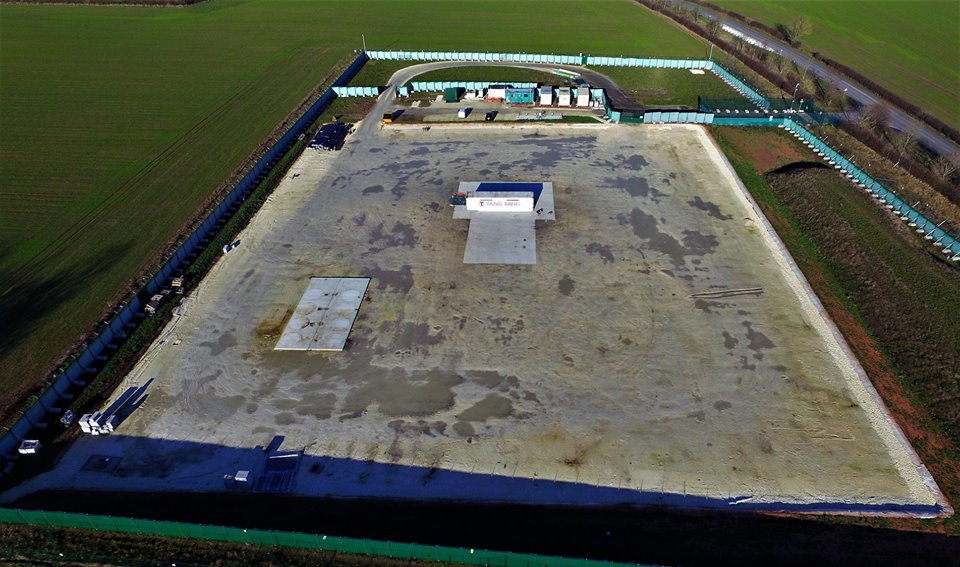

Tinker Lane, near Blyth, Nottinghamshire

IGas shale gas site at Tinker Lane, 28 January 2019. Photo: Eric Walton

The well, spudded on 27 November 2018, did not encounter the Bowland Shale. But IGas said in the accounts that preliminary tests on shale samples were “encouraging” for potential gas resources in the Gainsborough Trough basin. The analysis of these samples is still subject to further testing and validation, the company said.

Tinker Lane would help calibrate geological models of the region and demonstrated improvements in drilling performance, IGas said. It added:

“Preparations are being made to fully restore the site”.

Ellesmere Port, Cheshire

IGas site at Ellesmere Port, 21 January 2019. Photo: DrillOrDrop

A 12-day public inquiry held during January, February and March 2019 examined IGas’s appeal against refusal of permission to carry out flow testing at its Ellesmere Port well. Participants have made written submissions to the planning inspector, particularly on a High Court ruling that government support for shale gas was unlawfully included in the National Planning Policy Framework.

IGas said:

“No further activity in the PEDL licences that fall within the Cheshire West and Chester Council planning committee will be undertaken until the outcome of the Ellesmere Port appeal is known.”

Stockbridge, Hampshire

IGas said its Stockbridge project aimed to “debottleneck the water management constraints” to create additional production capacity and return existing wells to production.

It said there were successful results on four of five wells. A sidetrack, called STK19, had been drilled but it failed to provide the expected additional water injection capacity. The full benefit of the project could not be realised, IGas said. About 100 barrels of oil equivalent per day (boepd) remained shut-in. The company said:

“Measures are being pursued to unlock this additional potential and alleviate the water handling constraints.”

Albury, Surrey

IGas said electricity was exported to the grid from the Albury site in July 2018, four months ahead of schedule. The gas-to-grid project had been completed during the year and gas exported to the grid on schedule at the end of November 2018. Capability was now more than 170 boepd, the company said.

Welton, Lincolnshire

IGas said production capacity in the east midlands was constrained by water disposal. It said a project at Welton had resulted in an additional injection well and enhanced injection capacity. The next phase would begin early in 2019, the company said.

Block on licence sales

In May 2018, IGas announced it was seeking to sell 10 licences in the east midlands, southern England and north east Scotland to Onshore Petroleum Limited (OPL).

The company said today it was unlikely to get consent from Oil and Gas Authority (OGA). It said it was “in the process of exploring alternative options with OPL and the OGA as to the structure and form of a transaction.”

IGas had said it was seeking to divest from 100% licences from licences in Nottinghamshire (PL220, ML3, ML6, ML7), Hampshire (PEDL70) and West Sussex (PL205). It also wanted to divest 50% from PEDL158 on the Caithness coast in north east Scotland and an adjoining offshore licence and 25% from PEDL235 and PEDL257 in Surrey.

Key figures

Revenue: £42.9m; 2017: £35.8m

Earnings before interest, tax, depreciation and amortization: £10.8m; 2017 £9.2m

Underlying profit: £4m; 2017: £1.3m

Profit/(Loss) after tax: (£21.4m); 2017: £15.5m

Net debt: £6.4m; 2017: £6.2m

Cash balances: £15.1m; 2017: £15.7m

Net cash generated from operating activities: £12.9 million; 2017: £6.7 million

Cost of sales: £21.9m; 2017: £21.4m

Administrative expenses: £5.5m; 2017: £6.4m

Exploration expenses: £29.1m; 2017: £0.1m

Net average production: 2,258 barrels of oil equivalent per day (boepd); 2017: 2,335 boepd

Predicted production for 2019: 2,200-2,400 boepd

Operating costs: $31.9/barrels of oil equivalent (boe); 2017: $28.2/boe

Predicted operating costs in 2019: $32.5/boe

Net reserves

1P (proved): 9.78MMboe (thousand barrels of oil equivalent); 20178.11MMboe

2P (probable): 14.56 MMboe; 2017 13.64 MMboe

2C: 19.20 MMboe; 2017 22.21 MMboe

Categories: Industry

Looks as if recent predictions around consolidation and transfers in the on shore sector are playing out. Bit like N.Sea, but smaller scale.

Paul / Ruth / IGAS:

Something not right with this:

1P (proved): 9.78MMboe (thousand barrels of oil equivalent); 20178.11MMboe

Million BBls Oil Equivalent and a space between 2017 and 8.11?

Reserves on the increase?

MM is a million not a thousand