Gooseneck at Cuadrilla’s Preston New Road shale gas site, 5 August 2019. Photo: Ros Wills

In this guest post, anti-fracking campaigner and researcher, Ben Dean, argues that successive Conservative-led governments have failed to have full confidence in the onshore fracking industry.

I know David Cameron declared in 2014 that his coalition government was “going all out for shale”. And yes, in December 2015 ministers granted 93 new licences mainly for shale gas exploration.

There have also been written ministerial statements and policy revisions designed to streamline the planning system for fracking.

But I argue that in one crucial way Conservative administrations have proved they were not fully assured that onshore fracking would be successful.

The regulatory system established by government for the onshore industry has done little to ensure that operators actually explore and appraise shale gas reserves. And if you look at the numbers, the very limited onshore progress bears this out.

Since 2015, OGA data shows that offshore companies drilled nearly 600 wells. During the same period, onshore operators drilled 26. Of these, only five (including side-tracks) were for shale gas and just two were fracked, neither fully.

So, what’s the difference between the onshore and offshore legislative approaches? I argue it comes down mainly to a three-letter acronym.

MER

To make my case, I need to go back to the Conservative-led coalition government, in power from 2010-2015. Ministers were becoming concerned about declining production of oil and gas in the North Sea. Between 2010 and 2013, production fell 37%. Average production efficiency fell from 80% in 2004 to 60% in 2012 (source).

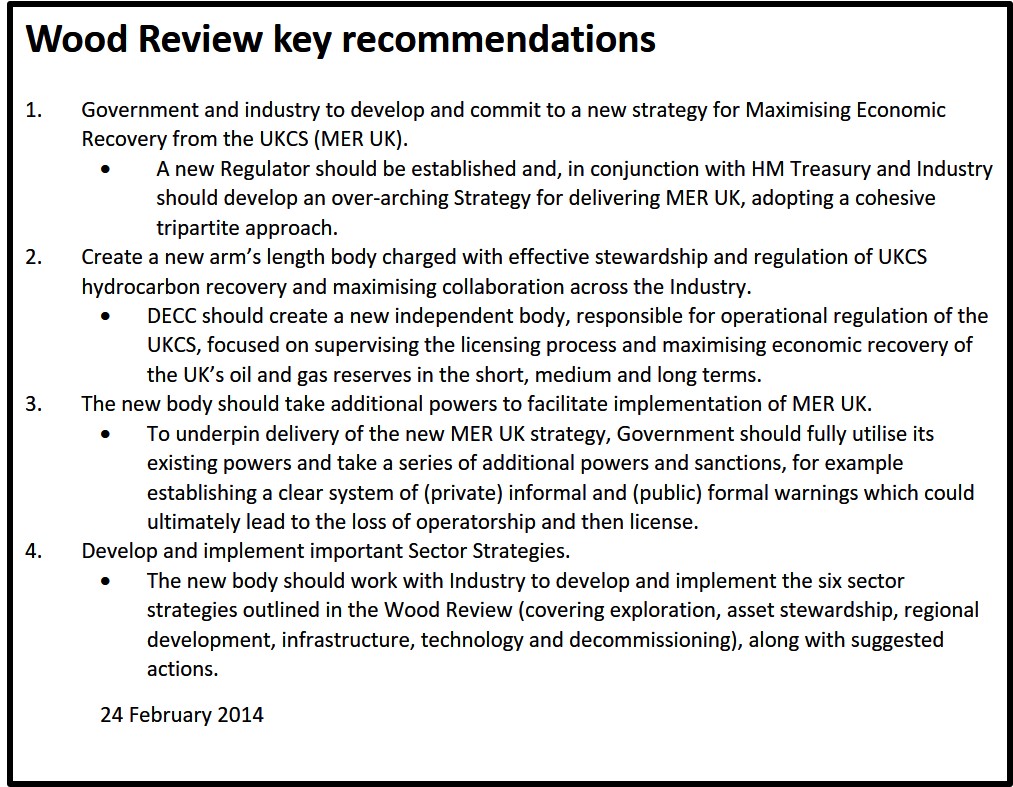

In June 2013, the coalition appointed the Scottish businessman, Sir Ian Wood, to conduct an independent review of how to maximise economic recovery of oil and gas offshore from the UK Continental Shelf.

The Wood Review was published in February 2014 and five months later the government accepted all the recommendations.

The Wood Review led to the Maximising Economic Recovery or MER strategy for UK offshore oil and gas (recommendation 1).

The MER UK Strategy came into force on 18 March 2016. Its central obligation was binding on the Oil & Gas Authority (OGA) and operators of oil and gas infrastructure, known as ‘relevant persons’. It stated:

“relevant persons must take the steps necessary to ensure that the maximum value of economically recoverable petroleum is recovered from the strata beneath UK waters.”

MER UK continues to apply to offshore licences but not to onshore equivalents. In a statement to DrillOrDrop, a spokesperson for the OGA said:

“I can confirm that the onshore oil and gas industry is not subject to the MER UK obligation.”

Any references in onshore planning applications or appeals to MER UK are wrong and invalid statements.

Offshore powers and sanctions

The Wood Review was also responsible for establishing the OGA (recommendation 2) and the 2016 Energy Act (recommendation 3).

Together, they set the UK offshore legislative framework and the regulations, including enforcement obligations and powers to implement MER.

Chapter 5 in part 2 of the Energy Act sets out the sanctions available to the OGA if the licence operator does not comply with MER UK or any other requirements.

The OGA has at its disposal ‘sanction notices’, which comprise enforcement notices, financial penalty notices, revocation notices or an operator removal notices.

Like MER, these sanction notices do not apply to onshore licences, the OGA confirmed in response to a freedom of information request.

Offshore licence are common law contracts that can be varied, deleted or added to if the parties agree. But the government gave the OGA legislative powers to manage offshore licences and increase production.

Regulating onshore licences

The same can’t be said for onshore licences.

They are also common law contracts that can, and are, regularly amended. But there is no MER obligation for licence operators and no sanction notices available to the OGA.

Since 2012, successive governments have failed to provide legislative assistance to enable the OGA to proactively manage onshore licenses. The consolidated onshore guidance, for example, has no reference to sanctions, enforcement or penalty.

As a result, the OGA is left in the weak position of being able to agree licence term extensions, work commitments and variations, which are generally meaningless.

The only other sanction open to the OGA is revocation of the licence. The OGA Overview 2019 refers to revocation of licences only in relation to offshore sanction notices and MER UK.

The single reference to revocation in the consolidated onshore guidance is where a licence holder buys or sells its stake without the OGA’s consent.

So does the OGA revoke licences for failure to comply with work commitments? I’m not aware of any public announcement of onshore revocations for this reason since the OGA was formed in 2015.

I argue that if the OGA started revoking licences for failure to meet work commitments there would be a flurry of requests to surrender from the operators.

There’s been very limited progress on work commitments by the companies granted licences in 2015.

In the 93 licences, no wells have yet been drilled or fracked and just two sites have so far been granted planning permission. Under the original work commitments, there are about 640 days left in which to drill 97 wells and frack 12. Meeting these commitments would require drilling at a rate of one well every six days.

Thanks to FOI requests, we know that some of the 2015 licence operators have already sought to vary their work programmes, well before the deadline of July 2021.

If the government believed the UK onshore fracking industry had a real chance of success, then surely, it would have applied MER UK and the relevant parts of the Energy Act to onshore licenses.

As it is the OGA is a weak and toothless regulator of the onshore fracking industry.

Silence on support for onshore fracking

Five years is a long time in fracking. In contrast to earlier vocal support for shale gas, ministers have recently gone quiet on the onshore industry.

The Queen’s Speech this week had no reference to shale gas or unconventional hydrocarbons.

Energy secretary, Andrea Leadsom, giving evidence to the select committee on 15 October 2019. Photo: Parliament TV

At a two-hour session before the business select committee yesterday, energy secretary Andrea Leadsom made no mention of onshore hydrocarbons, hydraulic fracturing or shale gas.

She briefly talked about hydrogen but mainly to production by electrolysis, rather than from hydrocarbons.

The government’s long-awaited energy white paper is now not expected until the first three months of 2020. And according to a recent report in the Sunday Times, it will prioritise renewable energy over fracking.

Ministers resisted lobbying from Cuadrilla and Ineos in autumn 2018 for a review of the traffic light system used to regulate seismic events induced by fracking.

There’s been no recent progress on the key proposals in a joint written ministerial statement issued in May 2018. The government consulted on treating non-fracking shale exploration as permitted development and including shale production in the Nationally Significant Infrastructure Project (NSIP) regime. But almost a year after the consultation closed the government has not reported the outcome.

And earlier this year, a high court judge quashed a revised paragraph in the National Planning Policy Framework that supported unconventional hydrocarbons. He ruled that the government carried out an unlawful public consultation on the revision and had failed to take account of scientific developments over low-carbon claims. There’s been no move to restore the policy.

Categories: Regulation

Hewes the Norwegian field is the Johan Sverdrup field. Nearly 3 billion BBLs recoverable and OPEX only a few $ per BBL. It is ironic that the Norwegian sovereign wealth fund is divesting out of hydrocarbons. Alan will approve as I doubt there is any fracking unless they are gravel packing.

Some pro-o&g Luddites need to realise change is happening, whether they like it or not.

Another government lack of support here. And a good and apposite quote –

“It has become clear in the course of these proceedings that environmental-impact assessment of offshore oil projects is still in the dark ages (in contrast to the planning system generally) and the 1999 Regulations need urgent amendment to bring them into the 21st century”.

https://divernet.com/2019/10/17/seahorse-diver-wins-government-climb-down/?

It will be interesting to see if the new environmental regs apply to the offshore wind and fishing industries Alan. I expect you would agree that tightening the regs is a good thing as is applying them to all offshore industries?

Alan Toothill

Change is certainly happening, but it’s not a black and white event.

The Sverdup field is an example of where a nation state has taken the decision to keep producing oil and gas, in quantities far beyond its own needs.

Chinese fracking is an example of a nation seeking to be on less dependant on imported hydrocarbons.

Both countries invest heavily in renewables. In China, You can drive for what seems hours, passing massive solar and wind farms. They also supply cheap solar panels to the world, as well as operating the worlds rare earth mining operations which enables the global move to renewables.

In Norway, they make the most of their hydropower.

Are these nation states luddites?

Meanwhile engineers continue to get on with moving to renewable power. From the same information source that provided information on the Sverdup field, here is an overview of energy storage, being the thorny issue of how to store renewables for non windy, rainy and for dull days.

https://www.fircroft.com/blogs/everything-you-need-to-know-about-energy-storage-systems-92891615551?utm_campaign=EngineeringPro+-+Issue+53+-+16th+October+2019+-+SH&utm_source=emailCampaign&utm_content=&utm_medium=email

Luddites were against the introduction of new technology, not a ban on the production of cotton.

Alan Toothill

Plus, good that the environmental regulations with regard to putting anything on the seabed, permanent or temporary should be fit for purpose, and that the gov has been challenged on this issue.

Be it a drill rig ( oil / gas etc ) wind turbine, embankment ( tidal ) or what have you.

https://windeurope.org/policy/topics/environment-planning/

Let’s draw bold strokes then, rather than being pedants trying to rely on techical arguments when every post by the pros here has been refuted in matters of fact.

The tide has turned. The days of the influence of the o&g industry on the UK government are over. IMO. It could not be otherwise given the climate emergency.

And to those Luddites who continue to argue the case for a morally bankrupt and soon to be financially bankrupt industry, as in the case of fracking –

“Your old road is rapidly agin’

Please get out of the new one

If you can’t lend your hand

For the times they are a-changin'”

Alan Toothill

Turning tides

The tide has turned for fossil fuel, it turned for coal a while ago, and shrinks for oil and gas as the overall UK oil and gas production industry shrinks. The Stone Age did not end due to a shortage of stone, or it’s use being banned. Better things came along. The annual BP report contains a number of predictions as to the near term growth and eventual decline in fossil fuel use globally. But it predicts that the production tide is still coming in, for a few years.

Days of influence

The days of-influence of the coal industry shrank dramatically once privatised, and then some more as CO2 targets were introduced. However it’s UK demise began in 1914.

The influence of the oil production industry industry on the UK government ( of any colour ) is not over, but it is shrinking in line with the reduction in UK fossil fuel production. Hence the comments re decommissioning and tax breaks here on DOD. It has more influence in Scotland than England I suspect.

The influence of the companies who sell oil and gas to the consumer remains. What influence Tesco, Morrison’s, Sainsbury’s ( cheapest in Lincoln today, but not if you spend £60 at Tesco and get 10p off per Litre ) Waitrose et al and all the small companies seeking to sell you energy ( gas or electricity ) is something I do not have a handle on.

The influence of industrial large users of fossil fuels remains ( Steel, Petrochemicals ), but a move from UK production to abroad would remove that.

The influence of mid size users ( from Amazon to Stobarts ) is still there. A point made almost daily re queues of Lorries at Dover re Brexit ( maybe we should glue on to the ferries ).

What influence the oil producing countries have on the UK government is a point to consider. As we import most of our imported oil and gas from Norway, they may have a major influence on any UK government in power, should they wish to exercise that influence.

Pedants and technical arguments

You say that every pro post on here has been refuted in matters of fact. I am not sure that is true. It only takes one post not refuted to falsify your hypothesis.

There has certainly been many a drawn out discussion as to matters of fact, and even more discussions as to the interpretation of those facts and opinions drawn from them. But on strict matters of fact there has been posts refuted in both camps.

However, if you are discussing matters of fact, does than not rely on pedantry and technical arguments to be refuted? Facts should not be refuted on uninformed opinion I guess.

Fracking

I have not heard anyone argue for fracking in the Fylde to restart recently on here. But good to see offshore wind doing well in the UK. Just need to work out how to store that energy. I am sure that the companies creating it will work on that, and some of those companies will be O&G majors ( but not oil and gas producing countries it seems unless anyone knows otherwise ).