Gooseneck at Cuadrilla’s Preston New Road shale gas site, 5 August 2019. Photo: Ros Wills

In this guest post, anti-fracking campaigner and researcher, Ben Dean, argues that successive Conservative-led governments have failed to have full confidence in the onshore fracking industry.

I know David Cameron declared in 2014 that his coalition government was “going all out for shale”. And yes, in December 2015 ministers granted 93 new licences mainly for shale gas exploration.

There have also been written ministerial statements and policy revisions designed to streamline the planning system for fracking.

But I argue that in one crucial way Conservative administrations have proved they were not fully assured that onshore fracking would be successful.

The regulatory system established by government for the onshore industry has done little to ensure that operators actually explore and appraise shale gas reserves. And if you look at the numbers, the very limited onshore progress bears this out.

Since 2015, OGA data shows that offshore companies drilled nearly 600 wells. During the same period, onshore operators drilled 26. Of these, only five (including side-tracks) were for shale gas and just two were fracked, neither fully.

So, what’s the difference between the onshore and offshore legislative approaches? I argue it comes down mainly to a three-letter acronym.

MER

To make my case, I need to go back to the Conservative-led coalition government, in power from 2010-2015. Ministers were becoming concerned about declining production of oil and gas in the North Sea. Between 2010 and 2013, production fell 37%. Average production efficiency fell from 80% in 2004 to 60% in 2012 (source).

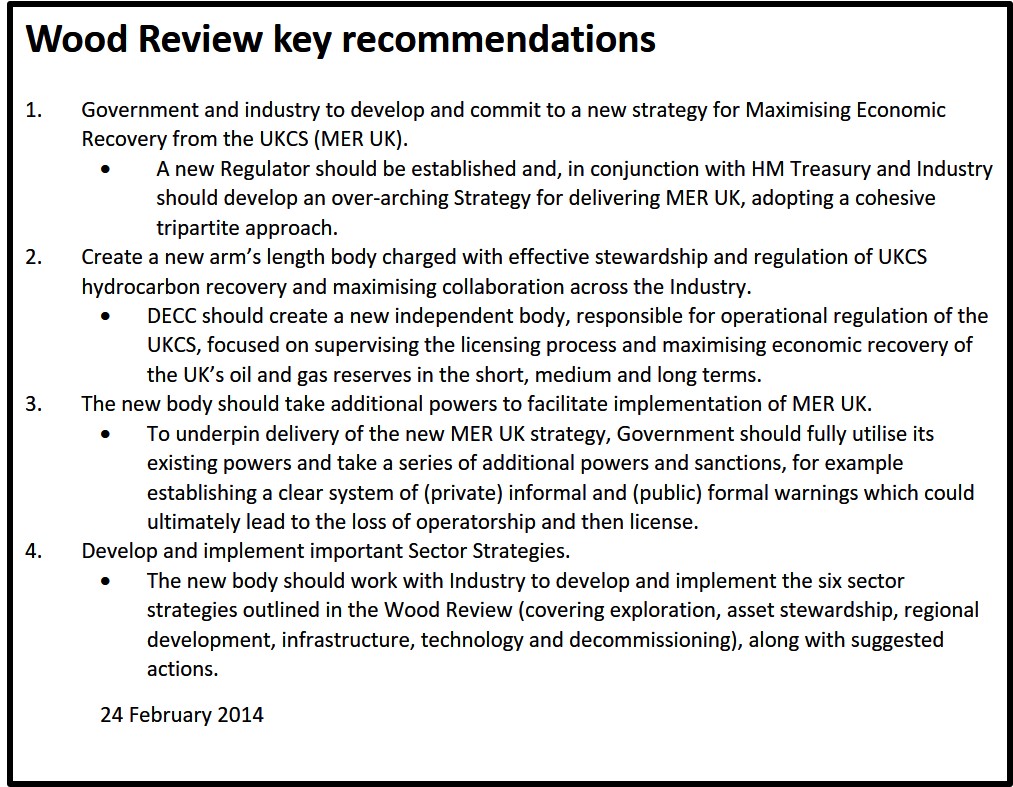

In June 2013, the coalition appointed the Scottish businessman, Sir Ian Wood, to conduct an independent review of how to maximise economic recovery of oil and gas offshore from the UK Continental Shelf.

The Wood Review was published in February 2014 and five months later the government accepted all the recommendations.

The Wood Review led to the Maximising Economic Recovery or MER strategy for UK offshore oil and gas (recommendation 1).

The MER UK Strategy came into force on 18 March 2016. Its central obligation was binding on the Oil & Gas Authority (OGA) and operators of oil and gas infrastructure, known as ‘relevant persons’. It stated:

“relevant persons must take the steps necessary to ensure that the maximum value of economically recoverable petroleum is recovered from the strata beneath UK waters.”

MER UK continues to apply to offshore licences but not to onshore equivalents. In a statement to DrillOrDrop, a spokesperson for the OGA said:

“I can confirm that the onshore oil and gas industry is not subject to the MER UK obligation.”

Any references in onshore planning applications or appeals to MER UK are wrong and invalid statements.

Offshore powers and sanctions

The Wood Review was also responsible for establishing the OGA (recommendation 2) and the 2016 Energy Act (recommendation 3).

Together, they set the UK offshore legislative framework and the regulations, including enforcement obligations and powers to implement MER.

Chapter 5 in part 2 of the Energy Act sets out the sanctions available to the OGA if the licence operator does not comply with MER UK or any other requirements.

The OGA has at its disposal ‘sanction notices’, which comprise enforcement notices, financial penalty notices, revocation notices or an operator removal notices.

Like MER, these sanction notices do not apply to onshore licences, the OGA confirmed in response to a freedom of information request.

Offshore licence are common law contracts that can be varied, deleted or added to if the parties agree. But the government gave the OGA legislative powers to manage offshore licences and increase production.

Regulating onshore licences

The same can’t be said for onshore licences.

They are also common law contracts that can, and are, regularly amended. But there is no MER obligation for licence operators and no sanction notices available to the OGA.

Since 2012, successive governments have failed to provide legislative assistance to enable the OGA to proactively manage onshore licenses. The consolidated onshore guidance, for example, has no reference to sanctions, enforcement or penalty.

As a result, the OGA is left in the weak position of being able to agree licence term extensions, work commitments and variations, which are generally meaningless.

The only other sanction open to the OGA is revocation of the licence. The OGA Overview 2019 refers to revocation of licences only in relation to offshore sanction notices and MER UK.

The single reference to revocation in the consolidated onshore guidance is where a licence holder buys or sells its stake without the OGA’s consent.

So does the OGA revoke licences for failure to comply with work commitments? I’m not aware of any public announcement of onshore revocations for this reason since the OGA was formed in 2015.

I argue that if the OGA started revoking licences for failure to meet work commitments there would be a flurry of requests to surrender from the operators.

There’s been very limited progress on work commitments by the companies granted licences in 2015.

In the 93 licences, no wells have yet been drilled or fracked and just two sites have so far been granted planning permission. Under the original work commitments, there are about 640 days left in which to drill 97 wells and frack 12. Meeting these commitments would require drilling at a rate of one well every six days.

Thanks to FOI requests, we know that some of the 2015 licence operators have already sought to vary their work programmes, well before the deadline of July 2021.

If the government believed the UK onshore fracking industry had a real chance of success, then surely, it would have applied MER UK and the relevant parts of the Energy Act to onshore licenses.

As it is the OGA is a weak and toothless regulator of the onshore fracking industry.

Silence on support for onshore fracking

Five years is a long time in fracking. In contrast to earlier vocal support for shale gas, ministers have recently gone quiet on the onshore industry.

The Queen’s Speech this week had no reference to shale gas or unconventional hydrocarbons.

Energy secretary, Andrea Leadsom, giving evidence to the select committee on 15 October 2019. Photo: Parliament TV

At a two-hour session before the business select committee yesterday, energy secretary Andrea Leadsom made no mention of onshore hydrocarbons, hydraulic fracturing or shale gas.

She briefly talked about hydrogen but mainly to production by electrolysis, rather than from hydrocarbons.

The government’s long-awaited energy white paper is now not expected until the first three months of 2020. And according to a recent report in the Sunday Times, it will prioritise renewable energy over fracking.

Ministers resisted lobbying from Cuadrilla and Ineos in autumn 2018 for a review of the traffic light system used to regulate seismic events induced by fracking.

There’s been no recent progress on the key proposals in a joint written ministerial statement issued in May 2018. The government consulted on treating non-fracking shale exploration as permitted development and including shale production in the Nationally Significant Infrastructure Project (NSIP) regime. But almost a year after the consultation closed the government has not reported the outcome.

And earlier this year, a high court judge quashed a revised paragraph in the National Planning Policy Framework that supported unconventional hydrocarbons. He ruled that the government carried out an unlawful public consultation on the revision and had failed to take account of scientific developments over low-carbon claims. There’s been no move to restore the policy.

Categories: Regulation

Not until tax revenue and energy security can be established.

Ermm-excuse me for stating the obvious, but is that not part of the testing objective which is no where near completed?

That will produce the usual speculation regarding whether that could be demonstrated, but I refer to the reality which has yet to be demonstrated but is still nothing to do with the speculation.

The reality is that the infliction of an unwanted dangerous industry on an unwilling host Community, first by stealth and flattery, then by bribery and propaganda, then by misuse of the local Constabulary and Judiciary system was never going to succeed in the long term .

Couple that with a poor choice of geographical location, riddled with existing faults and prone to flooding, the end of the Fylde fracking experiment is nigh.

However serious harm to local residents properties and relationships within the Community have been inflicted. More than likely the spreading of large amounts of cancer causing gaseous fracking byproducts will be proved in time to come to be also inflicted.

In the meantime Cuadrilla staff and their Contractors will have received millions of pounds from their gullible investors.

What a horrible destructive mess thanks to the foibles of human nature.

Thought you were talking about your former pay masters at first Peter?

I remember you saying you welcomed Bae on the Fylde Coast… Hmmm… You welcome an arms manufacturer but fight against an industry which will produce Gas to keep us warm and the lights on???

https://www.lep.co.uk/business/unmanned-aircraft-trials-stepped-up-by-bae-systems-1-8276442

That is significant, the clarification that MER does not apply to onshore.

In fact it should have been clear to us that the Infrastructure Act, as passed into law is clear on this. The devil is that it is in the last paragraph in the IA clause 41 amendments to the 1998 Petroleum Act section 9 where there is elucidation (this is the current version, not exactly the same as the enacted Bill text but near enough)

““UK petroleum” means petroleum which for the time being exists in its natural condition in strata beneath relevant UK waters;”

This specifically excludes onshore. This was reflected in the March 2016 OGA advice.

It is not surprising that some of us were misled. Through 2014 and into 2015 we raised the concern that the government was intending extending the Wood Report recommendations on MER to onshore. In July 2014 the government’s response to the Report stated

“The Government also believes that the MER UK philosophy established by Sir Ian’s Review should be applied to all oil and

gas recovery whether offshore in the UKCS or onshore.”

Exactly when the change of heart occurred I don’t know, and when that definition crept in to restrict MER to offshore. I suspect the government got into a fix because there was no yardstick for judging economic recovery due to fracking, so they just tore up the idea. I suspect many MPs didn’t know either.

Anyway mea culpa, Having commented on the outrage of the government attempting to use Wood to justify fracking support and onshore MER I should have checked what they eventually slipped into the technical details of the IA.

The episode probably suggests a lack of confidence in fracking in 2015. That could only be stronger now.

But yet advice to planners indeed continues to imply the requirement to maximise ALL UK production. West Sussex say (faqs January 2017)

“What is the national policy for energy (oil and gas)? National energy policy is that oil and gas make an essential contribution to the country’s prosperity and quality of life, and are important for energy security. While renewable energy must form an increasing part of the national energy picture, oil and gas remain key elements of the energy system for years to come. There is also a commitment to maximising indigenous resources (that is those which exist within the UK), subject to safety and environmental considerations.”

Industry has never thought MER / Wood applied to UK onshore. Onshore / offshore have always been treated separately, even the relevant industry bodies are different (UKOOA / UKOOG).

The point is, that many believed in 2014 that the government did intend to extend the maximisation to onshore. Unsurprising, because that’s what the government said, as you can read for yourself. It is irrelevant to say now that the industry never believed it would happen. But thanks, Paul, you are in fact just reinforcing Ben’s point.

Your point re different treatment is misleading, as evidenced by the creation of the OGA. It’s fracking obvious the industry divisions and interests are different. I am surprised there has been little vocal opposition to the offshore prospects for development including fracking.

Fear not, offshore, we expect Labour to continue its union-driven promotion of offshore O&G as per the 2017 manifesto. No split between the two major parties then, then. Feel free to also promote that.

The main reason that the focus, including MER, has been offshore is because that is where the reserves are. That is where the Governments’s revenue has come from. With the exception of Wytch Farm, there is not an onshore UK field of any reasonable size – hence the reason the majors all pull out in the 1980’s. We (I was with Amoco then) explored most of the UK and didn’t find reserves of sufficient size to be economic. We did find a lot of shale gas in Lancashire but of course this was before the exploitation processes of shale hydrocarbons had been developed. BP, Amoco and Conoco and probably others stopped exploring onshore UK around 30 years ago. This is why you only have small companies onshore UK now. Mostly set up for onshore UK PEDLs. They wouldn’t get licences offshore.

Why would there be any opposition to offshore development? Other than the usual BS from Greenpeas and Enemies of Industry most people support our offshore oil and gas industry – even your friend JP.

As far as I know there are no offshore shale developments anywhere in the world and there probably never will be. I expect even you can figure out why that is Alan? You really do have a chip on shoulder……

I have no issues with Ben’s article.

Interesting reference to Wytch Farm implying that it’s an onshore field. I was under the impression that it is just an onshore ‘tap point’ at the end of a very long well to an offshore field, due to refusal of permission for unsightly rigs spoiling the view from that millionaires paradise of Poole Harbour & Sandbanks. Is that not the case?

Mike Potter

Yes, the reservoir is mostly offshore ( of 3 ) but also partly onshore. However the above ground infrastructure is all onshore.

As you note, the extended reach wells were drilled to overcome objections and lack of permission for drill rigs and then subsea tie backs or small wellhead platforms.

However ….

The field is often called an onshore field in books, articles and the press ( as per below ).

https://www.hydrocarbons-technology.com/projects/wytch-farm-oil-field/

Maybe it’s just that the infrastructure being onshore, that it is termed as such rather than ‘onshore/ offshore’.

We never had an offshore coal industry, though many coastal pits worked out to sea. The NCB did once think of building a man made island off the coast and sinking a shaft or two, which would have been an offshore coal mine.

Wondering how impending Brexit will affect this?

Peter K

There will be no affect either way on how the present gov feels about fracking.

Which is ( as I see it ) to keep it all in the long grass and, unless something surprising turns up, let it die a natural death.

“Why would there be any opposition to offshore development?”

This must be pretty obvious, Paul. The prime need is to combat climate change. I care not whether offshore development is fracking, non-fracking, oil or gas. We do not need to maximise “UK” production we need to cut back in favour of alternatives. The MER is a disgraceful policy from a government pretending to pursue ambitious low-carbon objectives.

Personal abuse of Greenpeace by childish name-calling is unhelpful. And of me by talking of chips on shoulder. (?).

If you are convinced that there is no offshore fracking in the world you might search deeper. You could start by asking why there is controversy over the Trump administration’s issuing of licences and the fracking off California. Asking why there is opposition there – a second more localised environmental answer to your question. And you might ask why was the Trump administration was sued for letting oil companies dump offshore fracking waste Into the Gulf of Mexico? Admittedly the scope and kind of offshore fracking differs from onshore, but it happens.

Don’t take my word for it, from the horse’s mouth, eg

https://fuelfix.com/blog/2017/05/01/offshore-fracking-baker-hughes-builds-deep-water-tool/

And at other places around the world offshore fracking potential is a live issue.

In the UK we had licences issued for Morecambe Bay and off Blackpool. Yes (as happened onshore), contrary to another of your optimistic assertions, licences were given to cowboys with no experience. In this case Nebula Resources, which had in its founder a link to Cuadrilla. The brand new company was dissolved later that year (2014), unsurprisingly. The only surprise was that a licence was given them in the first place. So yes, UK offshore fracking may never happen, but it is the political will which is perhaps more important in deciding that than the technology. which exists and is working elsewhere. But the industry chancers may take a gamble. As the BBC said in 2014 “drilling offshore avoids the need for difficult negotiations with local councils, communities and landholders”. Dolphins and fish don’t have votes and don’t wave placards obstructing the rigs. Sadly.

I am glad you have no issues with Ben’s article. Neither do I. But it seems it saddens you. It heartens me. Far from having a chip on my shoulder I am now happy to have fought the right cause and we will sooner or later have the right result in a fracking ban.

Alan my comment relates to offhore shale development and the fracture stimulation of shales as being undertaken onshore around the world. The well density required will make it uneconomic. If you are referring to hydraulic fracture stimulation of conventional reservoirs offshore this has been going on for many decades. There are purpose built vessels to undertake this work. Many wells in the North Sea have been “fracked”. Offshore California fields are conventional reservoirs. I managed the largest offshore acid fracture stimulation in the world in the 1990’s (at that time) but the technique has been around since the 1940s. I don’t know when it was first used offshore, probably in the 1960s.

All reputable forecasts show global demand for oil and gas increasing for a while yet, oil peaking before gas, perhaps in the mid 2030s. UK North Sea reserves are depleting and imports increasing. Until we don’t need oil and and gas we should maximise our domestic production.

The UK is irrelevant to climate change. The developing middle classes in India / China / Asia and even Africa are where the increase in demand is coming from.

You said “As far as I know there are no offshore shale developments anywhere in the world”.

This is utter nonsense. Suck China, for a start. This displays either your ignorance or your duplicity.

Once again you shift your argument when what you have said is false. There is significant development offshore of shale. And significant fracking, As you now admit.

I will not respond to your other BS attempting to change the focus of the argument. [Edited by moderator]. However much you attempt to parade your antique past experience.

Alan offshore China shale oil play is news to me but it appears to be a 2019 development. Interesting but I expect it only works because it is in China. I look forward to your extensive list of offshore shale developments to further educate me. I also look forward to you referring this BB to where I have said there was no significant fracking offshore? And I still don’t believe there is “significant development offshore of shale”.

Not to worry, Google can never replace direct experience.

As for “climate change” – you brought this up not me. Or did you not re-read your post.

Good luck with whatever you are trying to achieve…….

Paul Tresco

Re Chinese offshore shale oil, it seems that CNPC are trying to develop shale oil near the Bohai Rim basin. This is a near shore / tidal project, as a small section of the basin is offshore.

https://www.reuters.com/article/us-china-cnpc-shale/cnpc-to-build-new-shale-oilfield-by-end-of-this-year-idUSKCN1QH0G2

It’s development has escaped the notice of world oil who report on the shale development in Jimsar, NW China, as China’s ‘first’ shale oil find. It produces 733bbl day.

https://www.worldoil.com/news/2019/2/19/chinese-oil-discovery-has-morgan-stanley-thinking-shale-boom

Morgan Stanley feel that Chinese shale oil production may get up to 100 – 200,000bbl day by 2025.

Given the geology for shale oil in China and its location I do not see any large offshore shale oil play developing.

Meanwhile, one Norwegian offshore oil and gas platform ( just in production ) can produce up to 600,000bbl day when on full production. That one platform alone can produce, on its own, three times that country’s demand for oil, and three to six times the expected production of shale oil in China by 2025.

So, as you note, given the high cost of offshore operations there is unlikely to be any boom in offshore shale oil or shale gas ( that needs HPHV fracking ) other than where political clout and cash drive it.

Especially as the cost of conventional offshore development drilling et al has been dropping.

https://oilprice.com/Energy/Energy-General/Is-Deepwater-Drilling-More-Profitable-Than-Shale.html

Thanks hewes. Perhaps Alan will let us know where all the other offshore shale production is?

Paul

Yes, it’s a monster. It only cost $10.5 billion

https://www.fircroft.com/blogs/first-oil-achieved-2-months-early-at-north-sea-johan-sverdrup-field-92807115744

Plus, of the £143 Billion profit it is a expected to make in its lifetime, £900 Billion will be trousered by the state. That means that Norway can spend lots on renewable energy development.

https://www.equinor.com/en/what-we-do/johan-sverdrup.html

The Norwegian SWF should divest out of hydrocarbons as, with oil revenue exceeding their budget, they need to diversify for they day oil goes out of fashion. You would not want all your eggs in one basket.