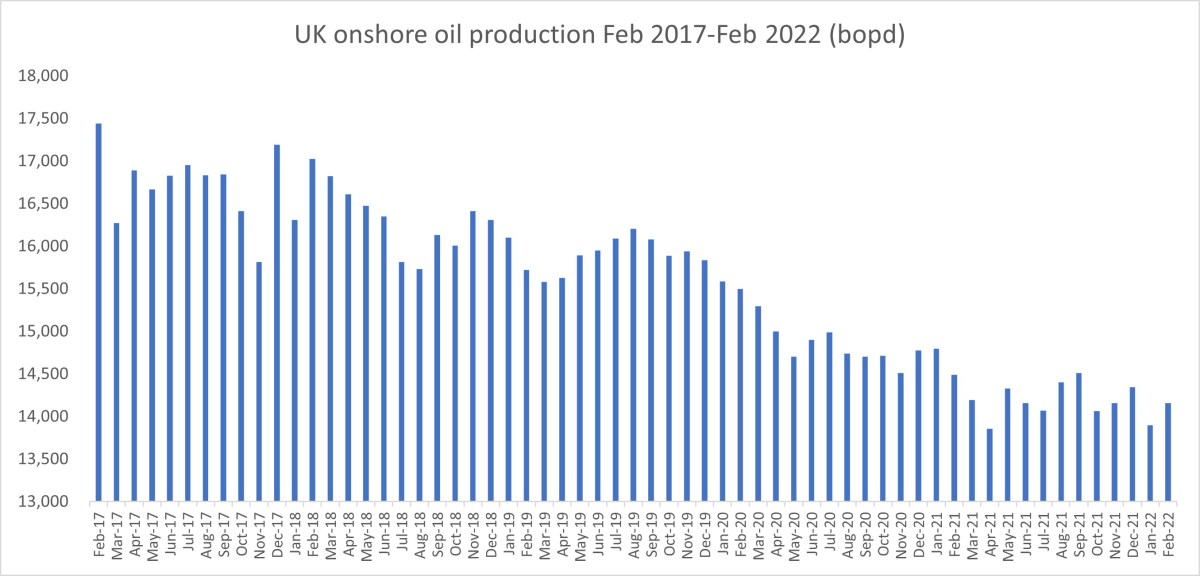

DrillOrDrop’s review of the latest UK onshore oil data for February 2022: small recovery in daily production but monthly volumes down

Key figures

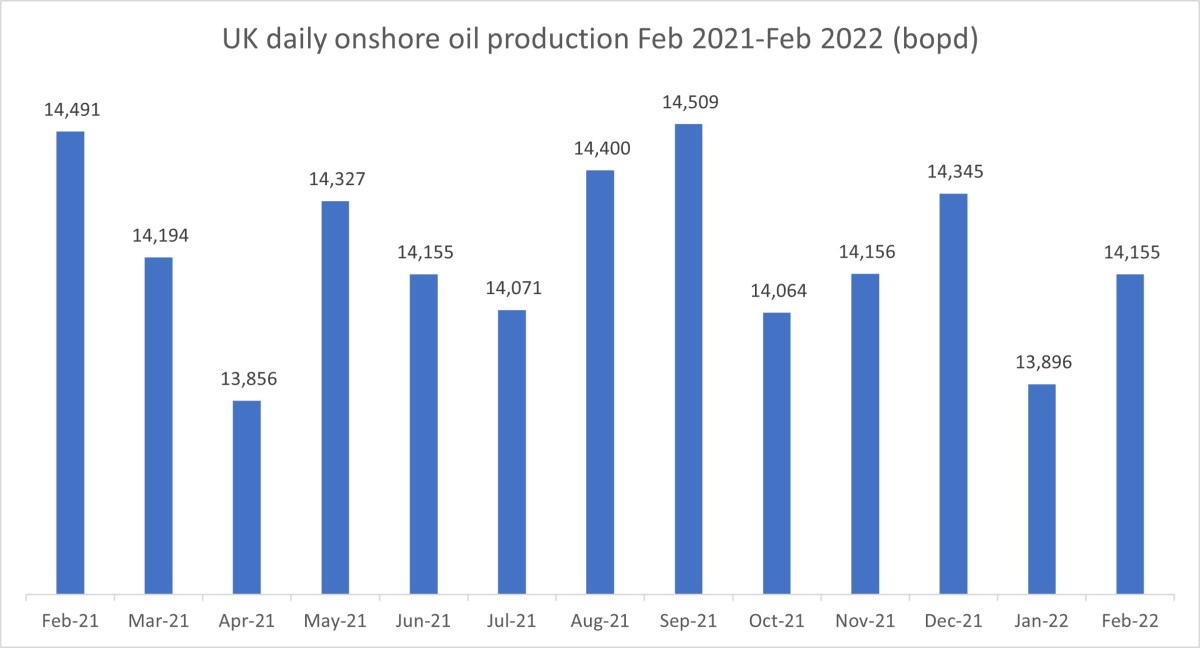

Daily production: 14,155 barrels per day (bopd)

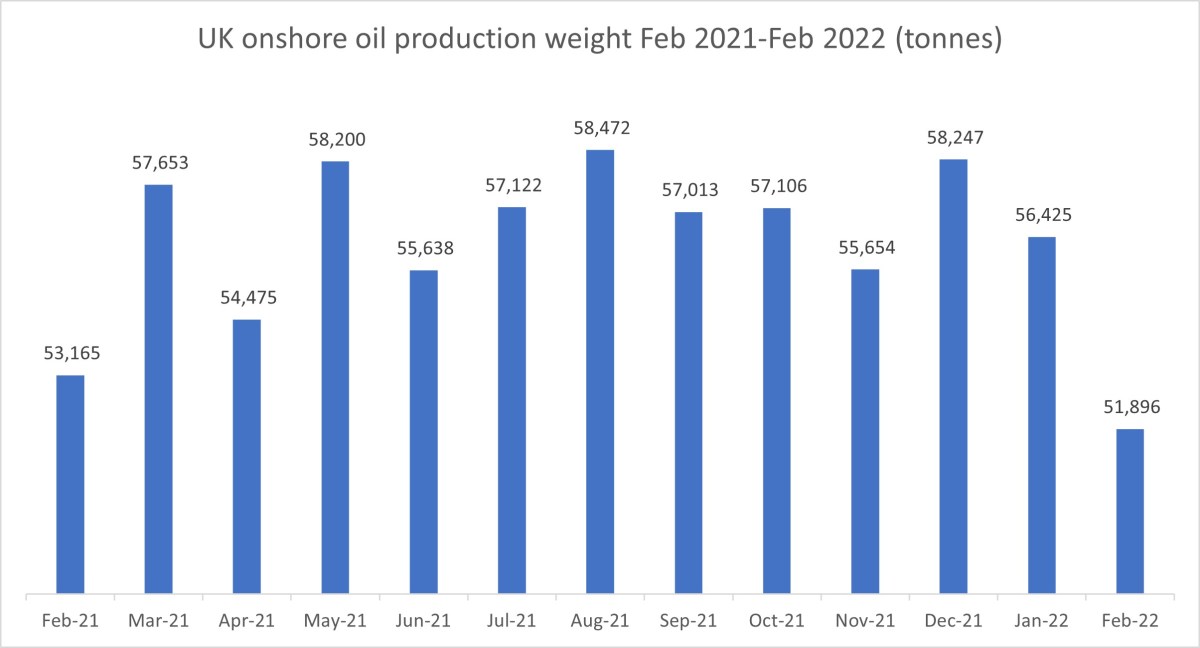

Weight: 51,896 tonnes

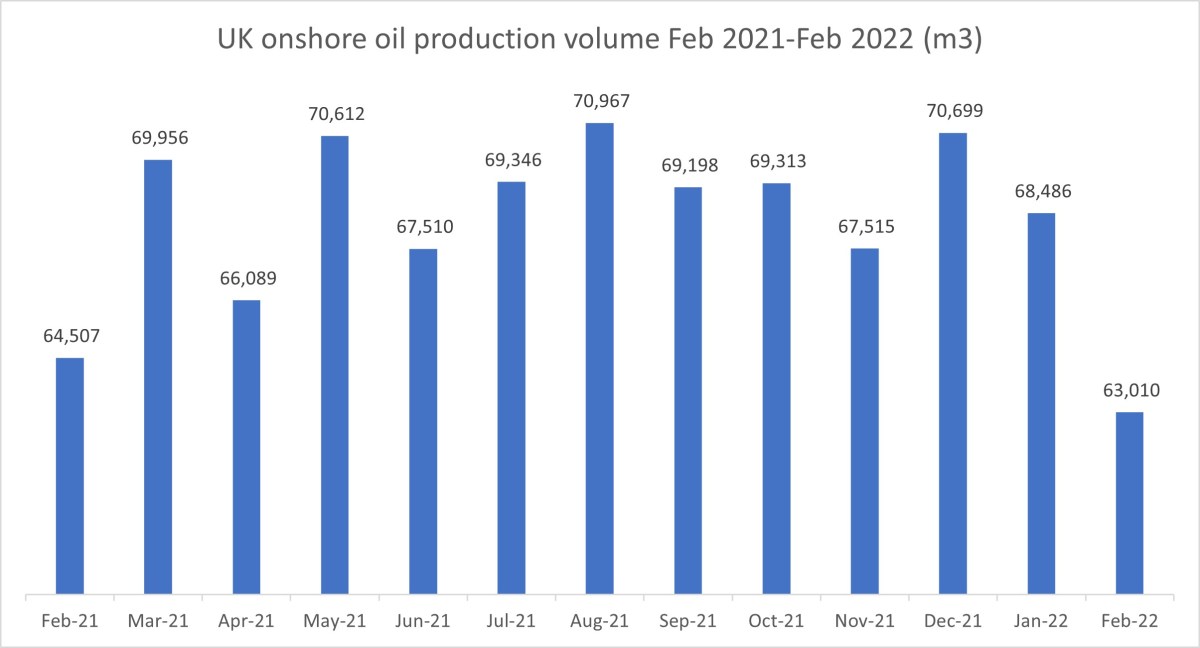

Volume: 63,010m3

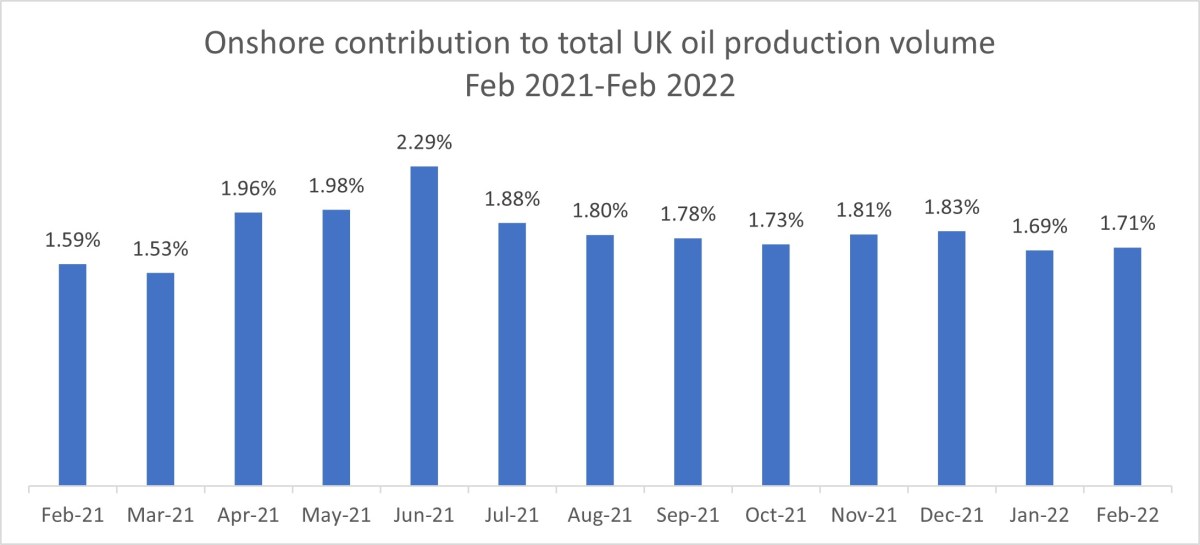

Volume of onshore as a proportion of UK total oil production: 1.71%

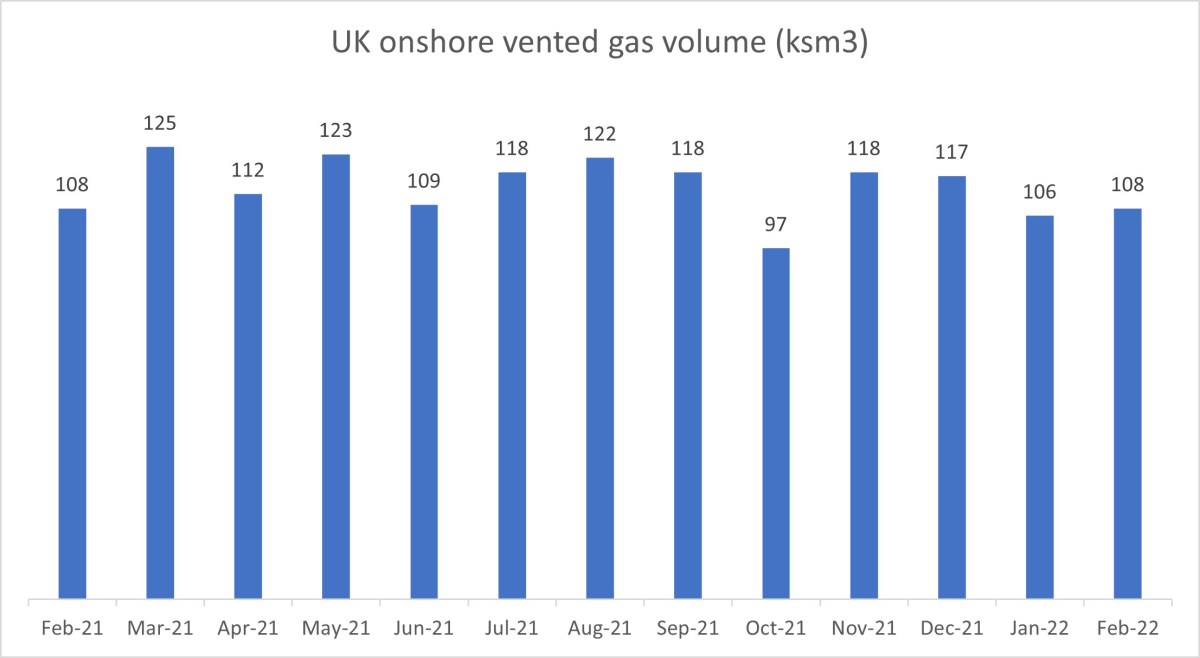

Volume of flared gas at UK onshore oilfields: 573 ksm3

Volume of vented gas at UK onshore oilfields: 108 ksm3

Headline of the month

Lowest monthly volume since February 2011 but small recovery in daily production after January 2022 fall.

The data in this post was compiled and published by the North Sea Transition Authority (NSTA) from reports by oil companies. It is published about three months in arrears. All the charts are based on the NSTA data.

Details

Daily production

- Total onshore barrels of oil per day (bopd) were up just over 1% from 14,010 barrels per day in January 2022. But daily production was more than 2% down on February 2021.

- February 2022 saw the joint fifth lowest daily production since Feb 2021.

Volume and weight

- Lowest monthly volume for 11 years

- Weight and volume were down just over 8% on January, probably reflecting the shorter month

- February 2022 was 2% down on February 2021 and 12% down on February 2020

Contribution to UK oil production volume

- The onshore contribution to total UK oil production was up marginally from 1.69% in January 2022 but remained the second lowest month since March 2021.

Flaring

- The volume of gas flared from UK onshore oil fields in February 2022 fell 16%, compared with January 2022.

- The percentage fall was about the double the drop in the volume of oil production.

- February 2022 continued a downward trend, which began in November 2021.

Venting

The volume of was gas vented by UK onshore oil fields rose almost 2% between January and February 2022. The monthly total, at 108 ksm3, was the same as in February 2021. It was below the average for the past year.

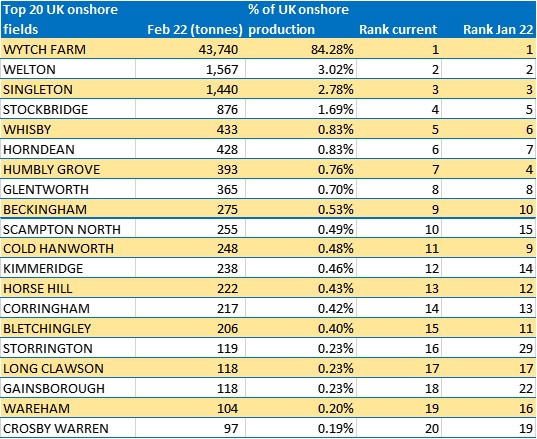

Top 20 fields

Six of the top 10 fields saw falls in production in February 2022, compared with January 2022

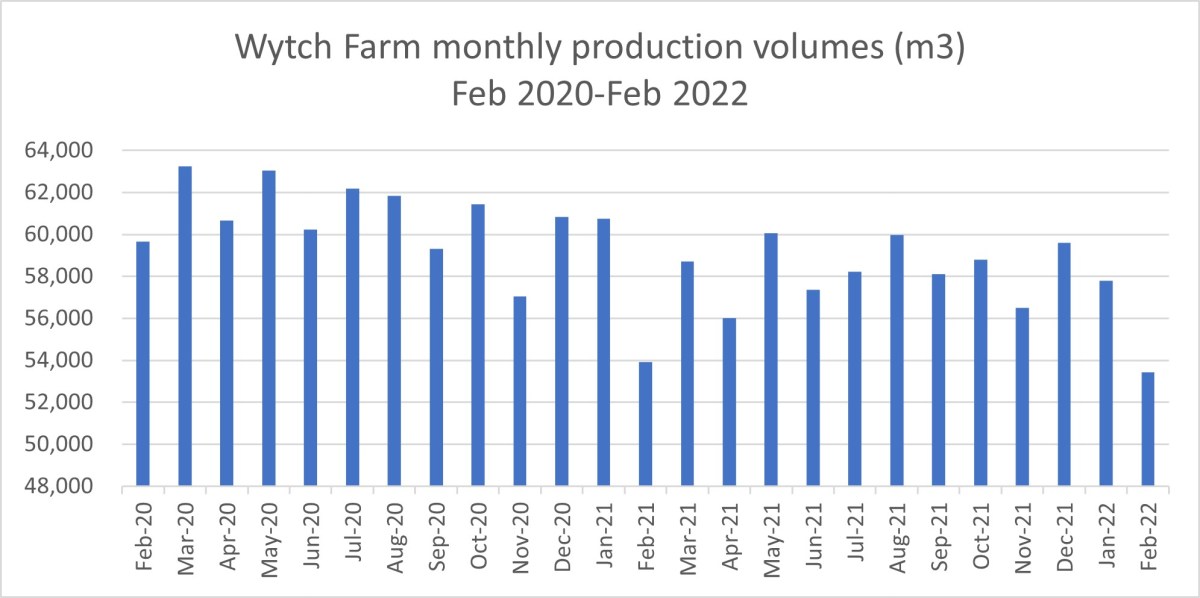

The biggest UK onshore producer, Wytch Farm, saw production drop to 53,439m3 in February 2022, its lowest monthly figure since September 2011. But daily production rose from 11,728 bopd in January 2022 to 12,004 bopd in February 2022.

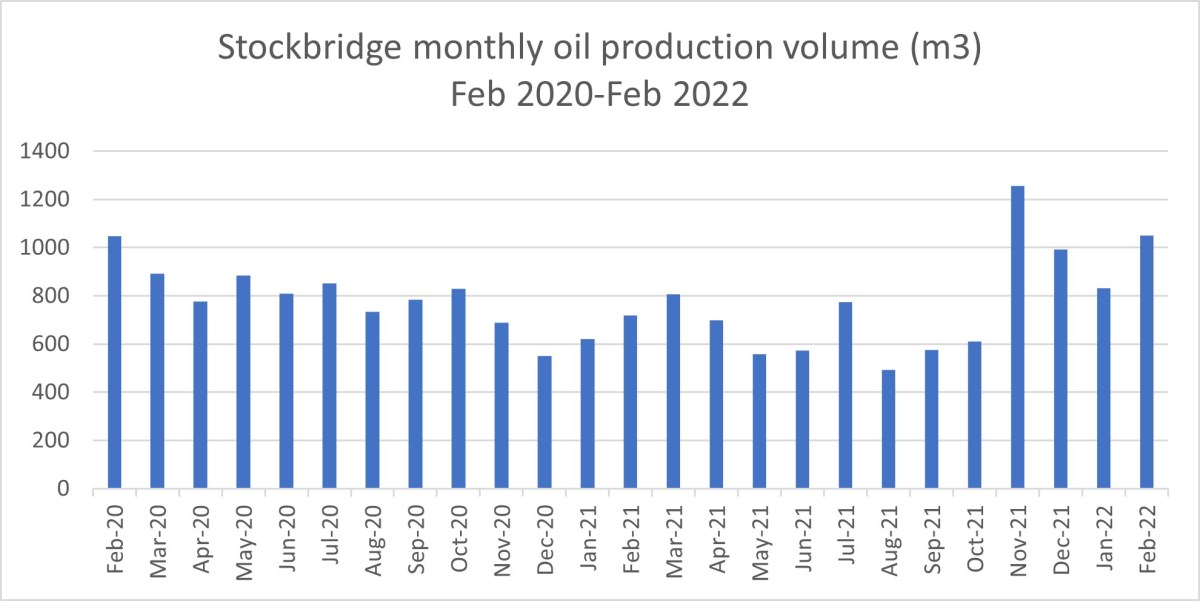

IGas sites at Singleton, Stockbridge and Scampton North all saw increases on the previous month

According to the data, Stockbridge reclaimed its fourth place in the rankings. Monthly volume at the field rose above 1,000m3 for only the third time in the past year.

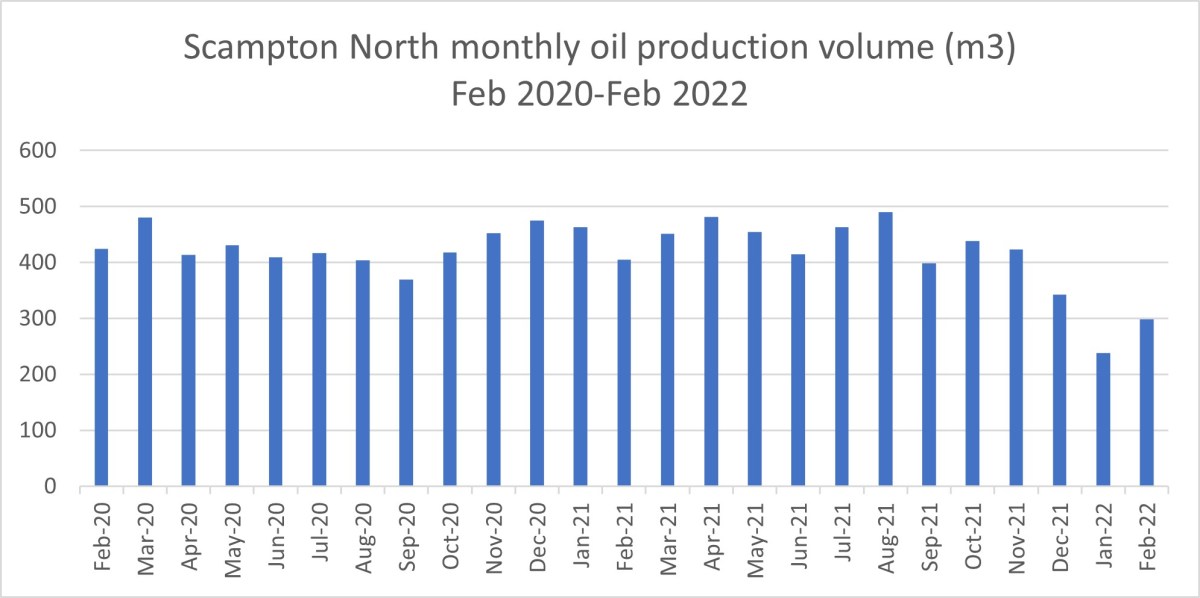

Scampton North rose to 10th from 15th in January 2022 with a 25% increase in production to 299m3 in February 2022. But February’s monthly volume was the third lowest recorded at the field, according to the data. Production rose in August 2020 after IGas began water reinjection at the field. But since August 2021, there have been four months of falling volumes.

Horse Hill fell another place to 13th. Monthly production dropped to 262m3, the lowest since September 2021, when production was suspended for several weeks. Daily production also fell slightly, from 60 bopd in January 2022 to 59 bopd. The volume of water production has fallen since October 2021, to 147m3 in February 2022.

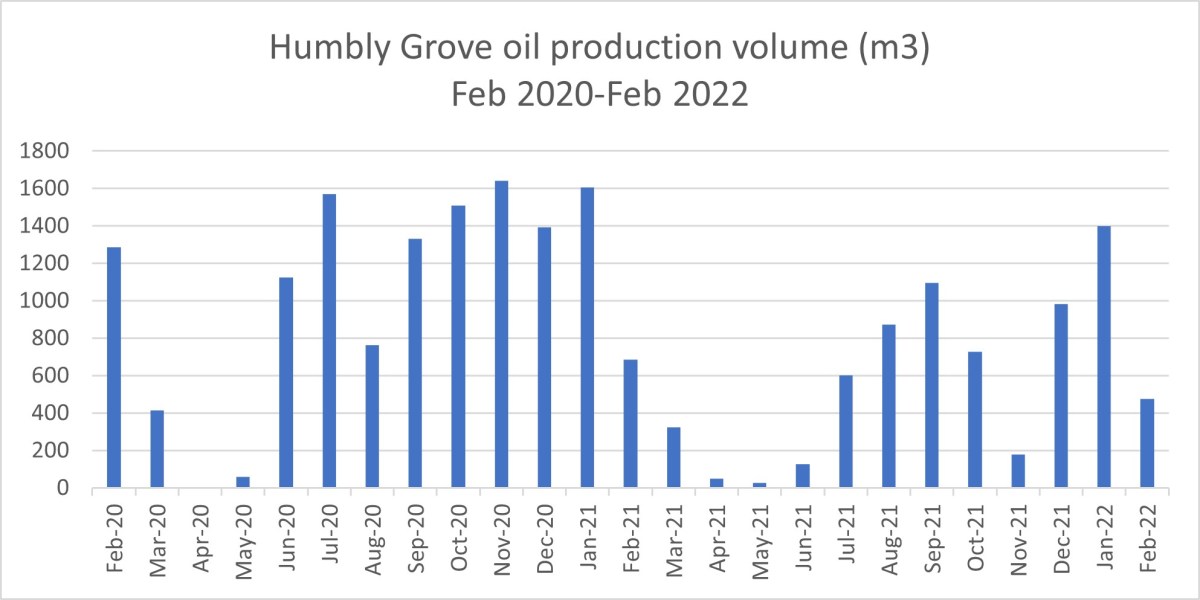

Variable production levels continued at Humbly Grove with volume down from 1,400m3 in January 2022 to 475m3 in February 2022. The field fell from 4th to 7th in top 20 rankings.

At Newton-on-Trent, the data has been altered since we last reported. The January 2022 release suggested the field had produced 480 tonnes, the first time in more than 10 years. In the February 2022 release, the data indicates that the field was still not producing.

No production

As well as Newton-on-Trent, there was also no production at Avington, Beckingham West, Egmanton, Scampton, South Leverton, Dukes Wood, Palmers Wood, Kirklington, Lidsey, Brockham, Waddock Cross and Nettleham.

With the NSTA correction for Newton-on-Trent, the non-producing fields remained the same as in January 2022.

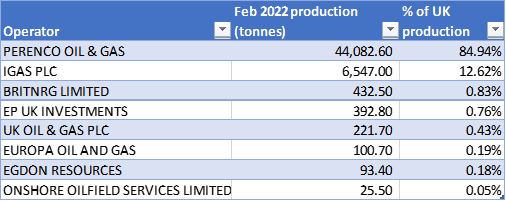

Operators

The UK’s biggest onshore operator, Perenco, again saw its total monthly production fall in February 2022, down 7.5% to 44,082 tonnes. The company’s contribution to UK onshore oil production rose slightly to 84.94%, up from 83.86% in January 2022.

Second-placed operator, IGas, saw production rise by 8 tonnes in February 2022, compared with the month before. Its contribution to UK onshore oil increased to 12.62% (January 2022 11.49%)

EP UK Investments saw its figure drop by more than 764 tonnes, with the fall in oil production at Humbly Grove.

February 2022 also saw falls in production for Egdon Resources and Europa Oil & Gas.

Egdon’s site at Wressle in North Lincolnshire remains under test and its production figures are not yet included in the data.

Breaking News:

February is a short month!

Not exactly the most radical reporting in recent times. More, first find a straw and then grasp it.

So that explains it all Martin, thank you for that information. I’m sure that a couple of days will make a lot of difference, it might push onshore oil close to 2% of UK production.

Well, Jono, it may already be there, as Wressle is not included.

But if you feel the level is so insignificant, then what is the problem? Would you be saying that UK production, as a whole, is not sufficient to meet UK demand, and therefore why bother at all and better to import the whole lot? And, if so, from where? And, then where would the lost taxation come from. Oh yes, the gullible. I quite like BP paying an extra £1 billion in taxes this year. Perhaps Rishi will not ask me for some more?

38Degrees

People Power and Change

Please Sign The Petition

It’s been a windfall week for the giant energy companies. BP and Shell announced profits of £12 billion in the first three months of 2022.

That’s £133 million a day or nearly £100,000 every minute. These excess (unearned) profits are driven largely by the war in Ukraine and surging energy prices.

To: Boris Johnson and Rishi Sunak

We need fair tax to tackle the cost of living crisis

https://you.38degrees.org.uk/petitions/we-need-fair-tax-to-tackle-the-cost-of-living-crisis?link_id=0&can_id=ab430bc601b1c6c806268b3d6ebe6c79&source=email-its-a-windfall-week-for-shell-and-bp&email_referrer=email_1534143&email_subject=its-a-windfall-week-for-shell-and-bp

Nope, PhilC

Not a chance.

More profit means already paying more tax, with enough left over to invest in net zero type investments-like £300B by 2030! I suspect Rishi will make sure that investment is made. Much better to get both, rather than only one.

By the way, you missed the bit about the hit both are taking by shedding their Russian investments. The war in Ukraine is actually driving the profits both ways! And the oil price was already surging prior to that war, and was a result of economies returning post Covid restrictions, creating more demand than could be easily supplied. But, you didn’t want it supplied at all, let alone easily!

How about those who have been wittering on about cheap renewable energy should put their hands in their pockets to compensate those that find it is not anything of the sort, and will have to pay out another £150B through their energy bills to get the nuclear as back up? How was that little gem missing from COP 26? Must have been submerged within stranded assets. Same people who have been wasting public money trying to stop UK production of oil and gas, in the Courts and within Planning, and now just see an opportunity to try another route of attack. Brass and neck come to mind, especially whilst that right to protest you support is being utilized to deliberately add cost to fuel distribution, that you now wish to be funded by those companies being targeted. Nope, increase the fines-let the culprits who add the cost pay the cost. And, £400K (Wressle costs) would help quite a few with energy bill issues. Have you started the crowd funding to repay that?

But, Sir Jim is willing to spend his money to try and bring more gas supplies on stream, and if successful would contribute some UK tax as a result. Perhaps I should start a petition for him to be given the green light? Or just get rid of the traffic lights? Or, £49k will buy one of his new vehicles, with a 3litre BMW diesel engine, so I could think of at least one buyer who may wish to contribute a bit of extra taxation.

38Degrees

People Power and Change

Please Don’t Sign The Petition

Actually these petitions are irrelevant and have zero influence on anything.

Another point of view:

https://www.agcc.co.uk/news-article/opinion-why-the-case-for-a-windfall-tax-misses-the-point

Welcome back to the fray, Paul. “We” missed you.

However. Following your own “logic”, the petition for a Windfall Tax on the fossil fuel industry, being “irrelevant” and having “zero influence” in your own opinion. There will be no harm whatsoever in signing the petition, will there?

So from that endorsement from Paul Tresto, everyone is now free to sign the petition.

Unless, of course, there is a good chance of the petition having the desired effect? Which is an even better reason to sign the petition, isn’t it. Maybe the only reason for that interjection is that there is a worrying chance that it will succeed?

So Paul says please sign the petition and then perhaps all will see what results emerge, now the recession has caused energy poverty and financial poverty in Great Britain.

Just for fun of course. What could go wrong?

Always a pleasure.

Ahh, “we” should sign a petition that “we” do not believe in, and is for nonsense? And, then Boaty McBoatface becomes valid?

Only, if “we” are all mad.

Maybe, but I am not. I do not sign anything I disagree with. Never have, never will.

Keep the golden geese laying those golden eggs, and encourage them to do so. Killing them off will simply remove the golden egg production. Shame the Dutch were also mad. LOL.

[Comments removed by moderator]