International efforts to replace gas supplies from Russia threaten the 1.5˚C warming limit, new analysis has shown.

If all the planned gas projects announced in response to the energy crisis are fulfilled, greenhouse gas emissions could add up to about 10% of the total carbon dioxide that can be emitted safely by 2050.

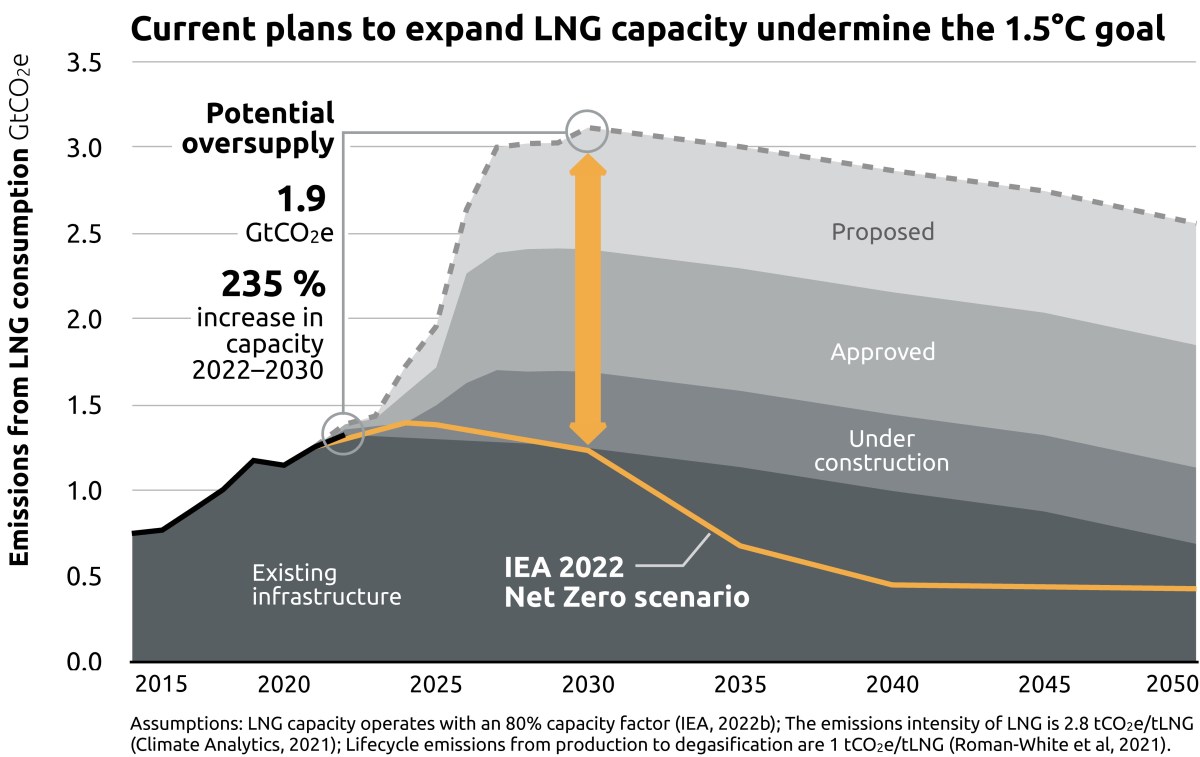

The analysis by Climate Action Tracker, released at COP27, found that in 2030 oversupply of liquified natural gas (LNG) could reach 500 megatonnes. This is equivalent to more than double total global Russian exports.

Climate Action Tracker said:

“This reaction to the energy crisis is an over reach that must be scaled back.”

The analysis showed that oversupply could lead to excess emissions of just under two gigatonnes of CO2 a year in 2030. This is well above the levels consistent with estimates produced by the International Energy Agency (IEA) to meet net zero by 2050.

Last year, the IEA warned that no new fossil fuel development could take place if the world were to stay within 1.5C of pre-industrial temperatures.

“The energy crisis has taken over the climate crisis, and our analysis shows proposed, approved and under construction LNG far exceeds what’s needed to replace Russian gas,” said Bill Hare, chief executive of the research institute, Climate Analytics, which along with NewClimate Institute forms Climate Action Tracker.

He said:

“We’re witnessing a major push for expanded fossil gas LNG production and import capacity across the world – in Europe, Africa, North America, Asia and Australia – which could cause global emissions to breach dangerous levels.

“Increasing our reliance on fossil gas cannot be the solution to today’s climate and energy crises anywhere.”

The analysis also predicted that global heating would reach 2.4C above pre-industrial levels by 2100, based on the policies agreed by governments so far. This is unchanged from the prediction at COP26, in Glasgow last year. The temperature predicted from the current policies pathway, which reflects action on the ground, remains at 2.7C.

If long-term net zero commitments were included, Climate Action Tracker predicted the temperature rise would be 1.8C.

The Intergovernmental Panel on Climate Change has forecast that 1.5C of warming would result in extreme heatwaves, rising sea levels and destruction of 70-90% of coral reefs.

Professor Niklas Hohne, of NewClimate Institute, said:

“With governments focussing on the energy crisis, this has been a year of little action on the climate: almost no updated national climate targets for 2030 and no significant increase in participation in Glasgow initiatives on coal phase out, clean cars and methane.”

Are they saying that Russian gas has less climate impact than gas from other areas? If you replace 1 Tcf of gas from Russian with 1 Tcf of gas from somewhere else, why is there such a huge increase in impact on climate change?

Perhaps: if there is oversupply, gas prices will fall and more gas will be burnt, either in the developed or developing world.

For example, falling gas prices may make gas-fired power generation more attractive, weakening the incentive to switch to renewables.

Gas was relatively cheap before Ukraine and this did not happen. We are not “Increasing our reliance on fossil gas”; we are making sure that Russian gas is replaced. The Greenies may think that Russian gas should not be replaced but they don’t offer viable alternatives and don’t appear to understand how the world works, and what people need and want.

“The energy crisis has taken over the climate crisis, and our analysis shows proposed, approved and under construction LNG far exceeds what’s needed to replace Russian gas,”

You can’t suddenly invent an LNG project to ship LNG, all these projects were already in progress. What you can do (Germany for example) is build an LNG import terminal so that you can replace Russian gas with imported gas from LNG exporting countries. It takes many years to explore for gas, appraise a discovery, confirm enough reserves (a lot) for an economic LNG scheme, and then develop the field and build the LNG export facilities.

Perhaps Climate Action Tracker could advise how to fix the Nord Stream Pipelines, negotiate a Russian withdrawal from Ukraine, and reinstate Russian gas exports?

https://www.nord-stream.com/

Paul

Its just a what if report. It would be good to add up all the in construction, approved and proposed fossil fuel producing activities and see where it lands. Even scarier I suspect. But approved and proposed does not mean will be built. The dynamics of the market will see to that I am sure. In addition, the graph does not take out russian gas or frack gas LNG. Is Frack gas not more sensitive to price variations? ie if the price falls, there is a lot lesss drilling?

Meanwhile, reuters report its boom time for coal mining projects, and worry about the same issues and stranded assets. Mind you, reuters picture shows a chap shovelling coal into a minecar (it says) is actually a chap working the minecar coupling. Always good to know the reporters know what they are talking about. If people had to hand shovel coal into minecars global coal production would be a fraction of what it actually is.

https://www.reuters.com/world/china/worlds-coal-producers-now-planning-more-than-400-new-mines-research-2021-06-03/

Supply creating demand, Paul T. Not simple replacement as argued ad nauseam by some arithmetically challenged contributors.

Nonsense, 1720. Elasticity of the equation is offered for those who are not already knowledgeable. If you want to ignore such, that is your choice. Maybe you dwell in N.Korea where that may still be the case, in Western Europe it is not. Hence Dutch TTF pay $47 per MMBtu for gas even though others enjoy $7 per MMBtu in USA. The demand is there in Europe, even at those prices, and supply will be brought/bought from other places to supply it. With all those transport emissions resulting from doing so. Something that will continue for decades yet.

For gas and oil, demand creates supply into Western Europe. Has been thus ever since maritime transport and pipelines were engineered to do so. If the current situation does not show that to everyone, then they are deluded or simply wanting to post fake news.

Intelligent people are expected to believe that in and around Wressle there is some sort of increase in demand because there is local supply. Really? Is there a queue of locals with their plastic buckets getting discounted oil? The concept is ludicrous. There are certainly some challenged contributors and it is interesting to note how willing they are to attempt to state what is nonsense, bypassing common sense, and then claim they represent a wider group.

.

With “friends” like that, good luck with being taken seriously but remember the Emperor’s New Clothes! Or, using a good old fossil fuel example, tarred with the same brush.

As you well know, Martyn, even with the usual levels of obtuseness characteristic of your postings, none, as far as I am aware, have ever argued that supply does not arise to meet demand. However, to argue, as you do, that the converse cannot be true, simply confirms my calling into question your claims to intellectual rigour.

[Edited at poster’s request]

I think I argued that the converse can be true for gas and oil-in N.Korea! Which confirms my calling into question your ability to read.

If the current situation in Europe, including UK, does not confirm the price elasticity for gas, then there are some who have no ability to apply any degree of intellectual rigour to the reality actually happening, here and now. The reason for that is obvious, and something that those knocking fossil fuels try to ignore-currently there is no practical, economical, widescale alternative to using gas. You can be as obtuse as you like, 1720, claim that is supported by others sharing such obtuseness, but it is obvious to everyone paying their energy bills, and seeing gas priced at $47 per MMBtu on the Dutch TTF and $7 per MMBtu on US Henry Hub yet with LNG tankers queuing to unload around Europe.

Once again you apply the failed approach to managing transition, trying to discard oil and gas before alternatives are ready to replace. If anyone wanted Net Zero to be discounted by humanity your approach is the one to go for where dogma overtakes commonsense. Come next April, when mass support to reduce energy bills will be removed, it will be interesting to see whether many share your myopia. For the politicians they will still find that most continue to heat, no matter what the price, but reduce expenditure on other things, reducing tax take. Therefore, it might actually be wise to encourage the fossil fuel companies to help towards transition, including Government tax take, because Governments will otherwise find themselves constrained in doing so by diverting tax to countries they are importing from, whilst having to cut foreign aid to them and others.

I am not holding my breath. The sudden realization that much more nuclear is needed in the UK is a pretty good indication of how good UK Governments are in managing any change within energy supply.

Paul Seaman that is!

As far as the UK is concerned we need gas through the transition. We have our own gas & should be producing it. Bringing in LNG increases lifecycle emissions dramatically. Polarised arguments generate easy slogans. It is lazy thinking. The facts are much more nuanced.

Here is the article about the additional emissions from importing LNG. https://www.bbc.co.uk/news/science-environment-63457377

When will analysts, activists and policy makers come clean on the fundamentals of the energy transition? They seem to forget the transition will make heavy demands on resource extraction and heavy industry, which require a huge amount of energy. Renewables cannot bootstrap themselves – they currently supply only a small single digit % of global needs .

If energy becomes expensive then so do the costs of renewable energy. The much touted price competitiveness of solar and wind infrastructure is largely down to the low price of coal in china, which is probably now history. We have seen how politicians privilege price support and supply to consumers rather than industry. Industry will starve, and the transition will falter.

The developing world is also demanding access to power, to lift comparably pitiful standards of living. They will use whatever sources they can, including coal – India has been vocal about that. Gas, including LNG, is a far better fuel in terms of pollution and GHG emissions than coal is. It’s such an obvious thing to pursue ALONGSIDE renewables development.

But better than LNG, with its liquefaction and shipping costs, is locally produced gas. Yes, fracked gas is more expensive to produce at source, but the equation is very different at point of delivery.

When will we have a proper debate that takes in all the factors that should influence an optimal energy policy? Currently it seems all we do is divide people into a scrum of opinions, between the polarities of belief and scepticism of prevailing narratives. driving many to take desperate but ultimately pointless measures. Perhaps it’s just politics?

Reblogged this on Wessex Solidarity.

From the Telegraph today:

“BP has begun shipping LNG from Mozambique.

First export shipment to set sail was hailed as a milestone for one of Africa’s poorest nations. (Except by the usual suspects!)

Left in an LNG tanker, called British Sponsor (how ironic!) bound for an unnamed European destination.”

Looks a bit like demand creating supply.